About

About

Online

Online

Data

Data

By CNBS Honduras

Financial inclusion is part of the strategic vision of the National Banking and Insurance Commission (CNBS) of Honduras and consistent with the Government Plan (2022-2026) of President Xiomara Castro. As a crucial component of the Central American nation’s economic growth, financial inclusion contributes to the reduction of poverty and inequality by providing citizens with access to basic financial products and services.

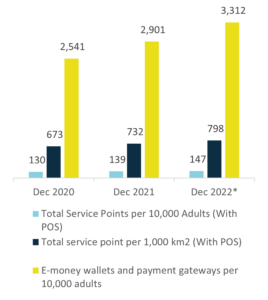

Graph 1 shows the main results of the inclusion strategies implemented by the institutions regulated by the CNBS. It indicates that in December 2022, access to service points with total POS (Point Of Sale) per 1,000 km2, registered an inter-annual growth of 9.0%, higher than the 8.8% observed the previous year. Additionally, the use of financial products and services1 showed an inter-annual growth of 16.4%, above that registered in the same period of 2021 (15.6% annually). Regarding digital and payment services, the total number of electronic wallets amounted to 1,664,449 at the end of 2022, growing by 18.3% per year, the same as that registered in the same period of 2021 (18.3%).

In addition, at the end of 2022, on average, for every 10,000 adults over 18 years of age, 3,312 wallets and payment gateways were registered – that’s 14.2% higher than that registered in 2021.

Graph 1: Significant Indicators of Financial Inclusion

Regulatory changes to promote financial inclusion in Honduras

In order to promote credit democratization, the Government of the Republic of Honduras approved regulatory measures aimed at reducing the permanence time of negative debtor information in the Credit Information Center (CIC). As of November 2022, a total of 238,193 people benefited from the new measures, 46% of which correspond to women.

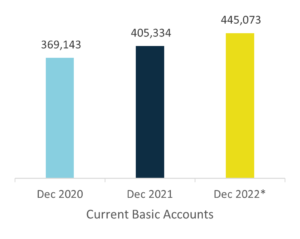

In the same way, reforms were made to the regulations administering the issuance of basic savings accounts in CNBS-supervised institutions. Graph 2 reveals that as of December 2022, basic savings accounts totaled 445,073, registering an annual growth of 9.8%, equal to that registered in the same period of 2021 (9.8%).

Graph 2: Behavior of Current Basic Accounts

In this way, the CNBS has promoted financial inclusion by simplifying requirements for access to appropriate financial products and services, thereby advancing economic participation (of residents and non-residents) and generating new opportunities for economic growth.

In this context, the new strategic approach of the CNBS aims to boost financial inclusion by taking advantage of the functionality of supervised systems, in order to close existing gaps in the availability and accessibility of financial products and services. In return, CNBS contributes to achieving a more stable, fair, transparent, and competitive economy by advancing the democratization of credit, promoting increased participation in the financial system, and reducing overall financial informality.

As a result, the CNBS expects that the implementation of financial inclusion policies will promote the economic and social development of all segments of society – especially in low-income and vulnerable communities – by improving living conditions, expanding opportunities, and supporting the activities of Micro, Small and Medium Enterprises (MSMEs). In addition, it aims to reverse the historic exclusion of certain segments of the population, by providing them with fair access to basic financial services.

© Alliance for Financial Inclusion 2009-2024