Maisa AbuBaker, Financial Inclusion Coordinator, Palestine Monetary Authority

When I saw the data from our national market study, one figure struck me: only one in five Palestinian women owned a bank account. This is not because branches are out of reach. Rather, it’s because they feel the formal financial system wasn’t built for them.

That recognition is what drives the work we have been doing at the Palestine Monetary Authority (PMA), and it is the story behind two new publications we are proud to share with the AFI community.

Two Studies, One Mission

In 2025, PMA completed two complementary pieces of research on women’s financial inclusion in Palestine. The first, a Market Study conducted across all Palestinian governorates, surveyed 1,132 women and produced the most detailed picture we have ever had of how women experience—and often avoid—formal financial services. The second, a Case Study, examines the barriers women face, and documents what PMA and Palestinian financial institutions have done to address them. It draws on global lessons from Egypt, Pakistan, Ecuador, Kenya, and beyond.

Together, they tell a story that is both sobering and hopeful.

The Numbers Behind the Gap

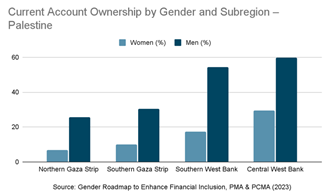

By end-2025, Palestine’s overall financial inclusion rate had reached 64%. But the gender divide is stark: 79% of men are financially included, compared to only 48% of women. Account ownership follows the same pattern (68% vs. 37%), as does access to credit, where men are three times more likely to hold a bank loan. Nearly half of all women said they could not access any funds in a financial crisis.

Why is this? Social norms play a powerful role. As one banker put it: “Financial institutions still don’t see women as a highly attractive segment but in fact, women have income and are often better savers than men.” The appetite is there. The formal products that match it largely are not.

What We Are Doing

Under the National Financial Inclusion Strategy (2023–2025), PMA has introduced gender-adjusted credit scoring, the Monshati platform for women entrepreneurs, zero-interest loans through the Istidama Fund, and awareness workshops which reached 500 women in 2025. Palestinian banks are also stepping up with tailored savings schemes, tiered credit models, and collateral-free financing for women.

The path forward requires a National Financial Education Strategy, mandatory sex-disaggregated data reporting, and digital financial services designed with women in mind.

The data gives us the diagnosis. The question now is whether we have the collective will to act on it. We invite AFI members to share your own experiences. Tell us what it would take, in your context, to ensure the financial system truly works for women.

ACCESS THE REPORTS: